Options Margin Requirements

Options Margin Overview

US Options Margin Requirements

For residents of the United States trading options:

- Rules-based margin

- Portfolio margin

The complete margin requirement details are listed in the sections below.

The following calculations apply only to Margin, IRA Margin and Cash or IRA Cash. See our Portfolio Margin section for US Options requirements in a Portfolio Margin account.

FINRA and the NYSE have imposed rules to limit small investor day trading. Customers that these organizations classify as Pattern Day Traders are subject to special Day Trading Restrictions for U.S. securities.

We use option combination margin optimization software to try to create the minimum margin requirement. However, due to the system requirements required to determine the optimal solution, we cannot always guarantee the optimal combination in all cases. Please note that we do not support option exercises, assignments or deliveries which may result in an account being non-compliant with margin requirements. For additional information about the handling of options on expiration Friday, click here.

Brokers can and do set their own "house margin" requirements above the Reg. T or statutory minimum. For option spreads in VIX securities, we may charge an additional minimum house margin requirement of USD 150. For option positions that meet the definition of a "universal" spread under CBOE Rule 10.3(a)(5), we may charge an additional house requirement of 102% of the net maximum market loss associated with the spread (i.e., net long option position price – net short option position price * 102%), if greater than the statutory requirement.

Option Strategies

The following tables show option margin requirements for each type of margin combination.

Note:

These formulas make use of the functions Maximum (x, y, ..), Minimum (x, y, ..) and If (x, y, z). The Maximum function returns the greatest value of all parameters separated by commas within the paranthesis. As an example, Maximum (500, 2000, 1500) would return the value 2000. The Minimum function returns the least value of all parameters separated by commas within the paranthesis. As an example, Minimum (500, 2000, 1500) would return the value of 500. The If function checks a condition and if true uses formula y and if false formula z. As an example If (20 < 0, 30, 60) would return the value 60.

Clients must have an account net liquidation value of at least USD 2,000 to establish or increase an existing uncovered options position.

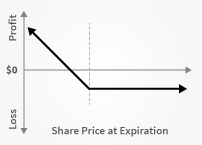

Long Call or Put

| Margin | |

| Initial/RegT End of Day Margin | None |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Initial |

| IRA Margin | Same as Margin Account |

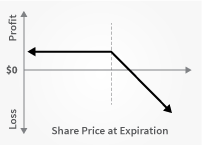

Short Naked Call

| Margin | |

| Initial/RegT End of Day Margin |

Stock Options 1, 2 Call Price + Maximum ((20% * Underlying Price - Out of the Money Amount), (10% * Underlying Price)) Index Options 1, 3 Call Price + Maximum ((15% * Underlying Price - Out of the Money Amount), (10% * Underlying Price)) World Currency Options 1, 2 Call Price + Maximum ((4% * Underlying Price - Out of the Money Amount), (0.75% * Underlying Price)) Cash Basket Option 1 In the Money Amount |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | Same as Cash Account |

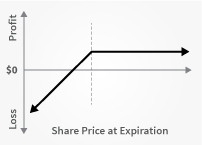

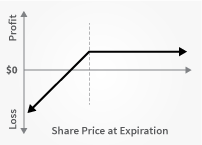

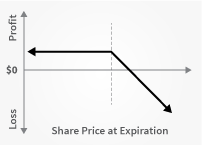

Short Naked Put

| Margin | |

| Initial/RegT End of Day Margin |

Stock Options 1, 2 Put Price + Maximum ((20% * Underlying Price - Out of the Money Amount), (10% * Strike Price)) Index Options 1, 3 Put Price + Maximum ((15% * Underlying Price - Out of the Money Amount), (10% * Strike Price)) World Currency Options 1, 2 Put Price + Maximum ((4% * Underlying Price - Out of the Money Amount), (0.75% * Underlying Price)) Cash Basket Option 1 In the Money Amount |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Put Strike Price |

| IRA Margin | Same as Cash Account |

Covered Calls

Short an option with an equity position held to cover full exercise upon assignment of the option contract.

| Margin | |

| Initial/RegT End of Day Margin | Max(Call Value, Long Stock Initial Margin) |

| Maintenance Margin | MAX[In-the-money amount + Margin(long stock evaluated at min(mark price, strike(short call))), min(stock value, max(call value, long stock margin))] |

| Cash or IRA Cash | Stock paid in full or None |

| IRA Margin | Stock paid in full or None |

Covered Puts

Short an option with an equity position held to cover full exercise upon assignment of the option contract.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement + In the Money Amount |

| Maintenance Margin | Initial Stock Margin Requirement + In the Money Amount |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Call Spread

A long and short position of equal number of calls on the same underlying (and same multiplier) if the long position expires on or after the short position.

| Margin | |

| Initial/RegT End of Day Margin | Maximum (Strike Long Call - Strike Short Call, 0) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Initial if both options are European-style cash-settled Otherwise, N/A. |

| IRA Margin | Same as Margin Account |

Put Spread

A long and short position of equal number of puts on the same underlying (and same multiplier) if the long position expires on or after the short position.

| Margin | |

| Initial/RegT End of Day Margin | Maximum (Short Put Strike - Long Put Strike, 0) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Margin Account (Both options must be European style cash settled) Short Put Strike Price (American style options) |

| IRA Margin | Same as Margin Account |

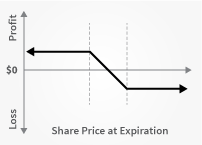

Collar

Long put and long underlying with short call. Put and call must have same expiration date, same underlying (and same multiplier), and put exercise price must be lower than call exercise price.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement + In the Money Call Amount Equity with Loan Value of Long Stock Minimum (Current Market Value, Call Aggregate Exercise Price) |

| Maintenance Margin | Minimum (((10% * Put Exercise Price) + Out of the-Money Put Amount), (25% * Call Exercise Price)) |

| Cash or IRA Cash | None |

| IRA Margin | None |

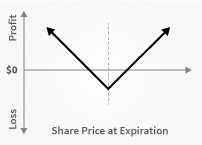

Long Call and Put

Buy a call and a put.

| Margin | |

| Initial/RegT End of Day Margin | Margined as two long options. |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Margin Account |

| IRA Margin | Same as Margin Account |

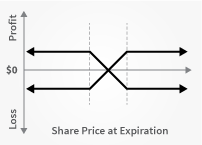

Short Call and Put

Sell a call and a put.

| Margin | |

| Initial/RegT End of Day Margin |

If Initial Margin Short Put > Initial Short Call, then Initial Margin Short Put + Price Short Call else If Initial Margin Short Call >= Initial Short Put, then Initial Margin Short Call + Price Short Put |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Long Butterfly

Two short options of the same series (class, multiplier, strike price, expiration) offset by one long option of the same type (put or call) with a higher strike price and one long option of the same type with a lower strike price. All component options must have the same expiration, same underlying, and intervals between exercise prices must be equal.

| Margin | |

| Initial/RegT End of Day Margin | None |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | None Both options must be European-style cash-settled. |

| IRA Margin | Same as Margin Account |

Short Butterfly Put

Two long put options of the same series offset by one short put option with a higher strike price and one short put option with a lower strike price. All component options must have the same expiration, same underlying, and intervals between exercise prices must be equal.

| Margin | |

| Initial/RegT End of Day Margin | MAX(Highest Put Strike - Middle Put Strike, 0) + MAX(Lowest Put Strike - Middle Put Strike, 0) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Short Butterfly Call

Two long call options of the same series offset by one short call option with a higher strike price and one short call option with a lower strike price. All component options must have the same expiration, same underlying, and intervals between exercise prices must be equal.

| Margin | |

| Initial/RegT End of Day Margin | MAX(Middle Call Options Strike - High Call Options Strike, 0) + MAX(Middle Call Options Strike - Lowest Call Option Strike, 0) |

| Maintenance Margin | Must maintain initial margin. |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Long Box Spread

Long call and short put with the same exercise price ("buy side") coupled with a long put and short call with the same exercise price ("sell side"). Buy side exercise price is lower than the sell side exercise price. All component options must have the same expiration, and underlying (multiplier).

| Margin | |

| Initial/RegT End of Day Margin | None |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | Same as Margin Account |

Short Box Spread

Long call and short put with the same exercise price ("buy side") coupled with a long put and short call with the same exercise price ("sell side"). Buy side exercise price is higher than the sell side exercise price. All component options must have the same expiration, and underlying (multiplier).

| Margin | |

| Initial/RegT End of Day Margin | MAX(1.02 x cost to close, Long Call Strike – Short Call Strike) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | Same as Margin Account |

Conversion

Long put and long underlying with short call. Put and call must have the same expiration date, underlying (multiplier), and exercise price.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement + In the Money Call Amount |

| Maintenance Margin | 10% of the strike price + In the Money Call Amount |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Reverse Conversion

Long call and short underlying with short put. Put and call must have same expiration date, underlying (multiplier), and exercise price.

| Margin | |

| Initial/RegT End of Day Margin | In the Money Put Amount + Initial Stock Margin Requirement |

| Maintenance Margin | In the Money Put Amount + (10% * Strike Price) |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Protective Put

Long Put and Long Underlying.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement |

| Maintenance Margin | Minimum (((10% * Put Strike Price) + Put Out of the Money Amount), Long Stock Maintenance Requirement) |

| Cash or IRA Cash | None |

| IRA Margin | None |

Protective Call

Long Call and Short Underlying.

| Margin | |

| Initial/RegT End of Day Margin | Initial Standard Stock Margin Requirement |

| Maintenance Margin | Minimum (((10% * Call Strike Price) + Call Out of the Money Amount), Short Stock Maintenance Requirement) |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Iron Condor

Sell a put, buy put, sell a call, buy a call.

| Margin | |

| Initial/RegT End of Day Margin | Short Put Strike - Long Put Strike |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | If all options are European and cash-settled, same as margin account. |

| IRA Margin | Same as Margin Account |

Overview of Pattern Day Trading ("PDT") Rules

FINRA and the NYSE have instituted regulations intended to limit the amount of trading that can be done in accounts with small amounts of capital, specifically accounts with less than 25,000 USD Net Liquidation Value. Pattern Day Trading rules will not apply to Portfolio Margin accounts.

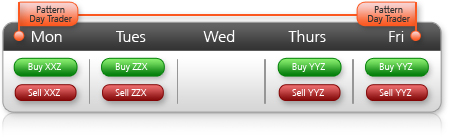

- Day Trade: any trade pair wherein a position in a security (Stocks, Stock and Index Options, Warrants, T-Bills, Bonds, or Single Stock Futures) is increased ("opened") and thereafter decreased ("closed") within the same trading session.

- Pattern Day Trader: someone who effects 4 or more Day Trades within a 5 business day period. A trader who executes 4 or more day trades in this time is deemed to be exhibiting a ‘pattern’ of day trading and is thereafter subject to the PDT restrictions.

- In order to day trade, the account must have at least 25,000 USD in Net Liquidation Value, where Net Liquidation Value includes cash, stocks, options, and futures P+L.

- The NYSE regulations state that if an account with less than 25,000 USD is flagged as a day trading account, the account must be frozen to prevent additional trades for a period of 90 days. We have created algorithms to prevent small accounts from being flagged as day trading accounts, to avoid triggering the 90 day freeze. We implement this by prohibiting the 4th opening transaction within 5 days if the account has less than 25,000 USD in equity.

Adjustments to Previous Day's Equity and First Day Trading

The previous day's equity is recorded at the close of the previous day (4:15 PM ET). Previous day's equity must be at least 25,000 USD. However, net deposits and withdrawals that brought the previous day's equity up to or greater than the required 25,000 USD after 4:15 PM ET on the previous trading day are handled as adjustments to the previous day's equity, so that on the next trading day, the customer is able to trade.

For example, suppose a new customer's deposit of 50,000 USD is received after the close of the trading day. Even though his previous day's equity was 0 at the close of the previous day, we handle the previous day's late deposit as an adjustment, and this customer's previous day equity is adjusted to 50,000 USD and he is able to trade on the first trading day. Without this adjustment, the customer's trades would be rejected on the first trading day based on the previous day's equity recorded at the close.

Special Cases

- Accounts that at one time had more than 25,000 USD, were identified as accounts with day trading activity, and thereafter the Net Liquidation Value in the account dropped below 25,000 USD, may find themselves subject to the 90 day trading restriction. The restrictions can be lifted by increasing the equity in the account or following the release procedure located in the Day Trading FAQ section.

- The proceeds of an option exercise or assignment will count towards day trading activity as if the underlying had been traded directly. Deliveries from single stock futures or lapse of options are not considered part of a day trading activity.

Additional details relating to PDT regulations and our implementation of these rules can be found in the FAQ section.

Day Trading FAQs

FINRA and the NYSE define a Pattern Day Trader (PDT) as one who effects four or more day trades (same day opening and closing of a given equity security ("stock") or equity option) within a five business day period.

Note that Futures contracts and Futures Options are not included in the SEC Day Trade rule.

A potential pattern day trader error message means that an account has less than the SEC required $25,000 minimum Net Liquidation Value AND the number of available day trades (3) has already been used within the last five days.

The system is programmed to prohibit any further trades to be initiated in the account, regardless of the intent to day trade that position or not. The system is programmed to protect the accounts with less than $25,000 so the account would not "potentially" be flagged as a day trading account.

If an account receives the error message "potential pattern day trader", there is no PDT flag to remove. The account holder will need to wait for the five-day period to end before any new positions can be initiated in the account.

The customer has the following options:

- Deposit funds to bring the account's equity up to the SEC required minimum of $25,000

- Wait the required 90 day period before any new positions can be initiated

- Request a PDT account reset

If the intraday situation occurs, the customer will immediately be prohibited from initiating any new positions. Customers should be able to close any existing positions in his account, but will not be allowed to initiate any new positions.

The customer will have the same options listed above, however, if at any time the Net Liquidation Value figure goes back above the threshold amount ($25,000), then the account will once again have unlimited day trades available.

FINRA has provided brokerage firms the ability to remove the PDT flag from a customer's account once every 180 days. If an account was erroneously flagged, and the customer's intent is not to day trade in his/her account, we have the ability to remove this flag. Once the PDT flag is removed, the customer will then be allowed three day trades every five business days. If an account gets re-flagged as a PDT account within 180 days after the reset, the customer then has the following options:

- Deposit funds to bring the account's equity up to the SEC required minimum of $25,000

- Wait the required 90 day period before any new positions can be initiated

FINRA and the NYSE define a Pattern Day Trader (PDT) as one who effects 4 or more day trades (same day purchase and sale of a given equity security ("stock") or equity option) within a five-day period, and NYSE and FINRA rules place certain restrictions on those who are deemed to be pattern day traders. If a customer account effects three (3) day trades involving stocks or equity options within any five (5) day period, we will require that such account satisfy the minimum Net Liquidation Value requirement of $25,000 before we will accept the next order to purchase or sell a stock or equity option. Once the account has effected a fourth day trade (in such 5 day period), we will deem the account to be a PDT account.

Pattern Day Trading regulations allow a broker to remove the PDT designation if the client acknowledges that she/he does not intend to engage in day trading strategies, and requests that the PDT designation be removed. If you wish to have the PDT designation for your account removed, provide us with the following information in a letter using the Customer Service Message Center in Account Management:

- Provide the following acknowledgements:

- I do not intend to engage in a day trading strategy in my account.

- I hereby request that you the broker no longer designate my account as a "Pattern Day Trading" account under NYSE and FINRA rules.

- I understand that if, following this acknowledgement I engage in Pattern Day Trading, my account will be designated as a Pattern Day Trading" account, and you the broker will apply all applicable PDT rules to my account.

- Log into Account Management, then click Message Center in the Support menu. Create a ticket in the Message Center, then paste the aforementioned acknowledgements, your account number, your name, and the statement "I agree" into the ticket form. Submit the ticket to Customer Service.

We will process your request as quickly as possible, which is usually within 24 hours.

For example, if the window reads (0,0,1,2,3), here is how to interpret this information:

If today was Wednesday, the first number within the parenthesis, 0, means that 0-day trades are available on Wednesday. The 2nd number in the parenthesis, 0, means that no day trades are available on Thursday. The 3rd number within the parenthesis, 1, means that on Friday 1-day trade is available. The 4th number within the parenthesis, 2, means that on Monday, if 1-day trade was not used on Friday, and then on Monday, the account would have 2-day trades available. The 5th number within the parenthesis, 3, means that if no day trades were used on either Friday or Monday, then on Tuesday, the account would have 3-day trades available.

Additional US Margin Requirements

For Residents of the United States:

Use the following links to view other margin requirements:

You can change your location setting by clicking here

Disclosures

- Minimum charge of USD 2.50 per share of underlying. This minimum does not apply for End of Day Reg T calculation purposes.

- For Leverage Options, Minimum (20% * Leverage Factor, 100%).

- For Leverage Options, Minimum (15% * Leverage Factor, 100%)

- For Covered Basket Calls, (short basket call, long component stocks), the margin requirement is for all the component stocks.

- Specific options with commodity-like behavior, such as VIX Index Options, have special spread rules and, consequently, may be required to meet higher margin requirements than a straightforward US equity option. Clients are urged to use the paper trading account to simulate an options spread in order to check the current margin on such spread.

- If a combination of options is put on in such a way that a specific strategy is optimal at that point in time, the strategy may remain in place until the account is revalued even if it does not remain the optimal strategy. A revaluation will occur when there is a position change within that symbol. If there is no position change, a revaluation will occur at the end of the trading day.

- Interactive Brokers Australia currently offers margin lending to all clients EXCEPT Self- managed Superannuation Fund account holders ("SMSF"). Click here for more information. For clients of Interactive Brokers Australia who are classified as retail, margin loans will be capped at AUD$25,000 (subject to change in IBKR Australia’s sole discretion). Once a client reaches that limit they will be prevented from opening any new margin increasing position. Closing or margin-reducing trades will be allowed.

- IBKR house margin requirements may be greater than rule-based margin.